Plan holders can use up to a maximum of $10,000 to pay for K-12 tuition from public, private, or religious institutions per beneficiary each year—penalty- and tax-free. Besides, how much can you put into an education IRA each year?

Special Considerations. Education IRAs have many conditions and stipulations, such as: Tax law prohibits funding an ESA once the beneficiary reaches 18 years old. Coverdell ESAs have an annual contribution limit of $2,000, but a penalty may be assessed if a plan holder exceeds that amount.

Also, are Education IRA contributions tax deductible? Coverdell ESA contributions are not tax deductible, but, like a Roth IRA, amounts deposited in the accounts grow tax-free until withdrawn. Withdrawals from Coverdell ESAs generally are tax-free to the extent that the amount of the withdrawal is not more than the beneficiary's qualified education expenses.

In this regard, what is the maximum contribution to a Coverdell Education Savings Account?

$2,000

What can you use an education IRA for?

Contributions. A Coverdell Education Savings Account or Coverdell ESA* (formerly known as an Education IRA) is a custodial saving account used for paying educational expenses. Taxpayers may make nondeductible cash contributions of up to $2000 a year for each child under age 18 (or for a special needs beneficiary).

Related Question Answers

Is it better for a parent or grandparent to own a 529 plan?

How Grandparent 529 Plans Affect Financial Aid. Overall, 529 plans have a minimal effect on financial aid. But, the FAFSA treats parent-owned accounts more favorably. For example, you report 529 plans assets as parent assets, which can only reduce aid eligibility by a maximum 5.64% of the account value. Can I use my IRA for tuition?

With funds from an IRA, a parent or student can pay for what are known as qualified education expenses – tuition, fees, books, supplies and equipment required for enrollment or attendance – without facing the penalty. How do I cash out my IRA for education?

- Complete a Coverdell ESA distribution request form from the financial institution that holds the Coverdell ESA.

- Submit the withdrawal request to the financial institution.

- Spend the proceeds on qualified education costs to avoid taxation.

Is a 529 tax deductible?

Never are 529 contributions tax deductible on the federal level. Earnings from 529 plans are not subject to federal tax and generally not subject to state tax when used for qualified education expenses such as tuition, fees, books, as well as room and board. How much can I put in 529 per year?

$15,000

How much can you contribute to a 529 plan in 2021?

In 2021, individuals can contribute up to $15,000 per beneficiary ($30,000 for gifts from a married couple) without using up part of their lifetime gift tax exemption or having to pay gift taxes. What happens to unused Coverdell funds?

If you have unused funds in a Coverdell ESA, they must be used or rolled over into another ESA or a 529 plan by the time the beneficiary reaches the age of 30 — or you can change the beneficiary on the existing account. Is Coverdell better than 529?

Coverdell education savings accounts provide more flexibility in investment choices, allowing investors to invest in individual stocks. 529 plans provide a limited number of stock and bond mutual funds, but also offer age-based asset allocations. Is there an age limit on 529 plans?

There are no time or age limits on using a state 529 college savings plan. Money can be kept in a 529 plan indefinitely. 529 plans can be used for graduate school, not just undergraduate school, and can be passed on to one's children. There is also no age limit on contributions to a 529 plan. What is the best account for college savings?

But 529s and ESAs are generally considered better choices for college savings because of their tax advantages. There are two types of tax-advantaged college savings plans designed to help parents finance education: 529 Plans and Education Savings Accounts (also known as ESAs or Coverdell accounts). What is the income limit for a Coverdell?

Income eligibility limit for contributors†Annual contributions for single filers are capped at $2,000 for MAGI up to $95,000, and are phased out for MAGI between $95,000 and $110,000. ‡Gift taxes may apply if you contribute more than $15,000 per year ($30,000 for couples).

Who can contribute to a CESA?

CESA Income Limits In 2020, you are able to make a full contribution if your modified adjusted gross income (MAGI) is less than $95,000 (single filer) or less than $190,000 if married filing jointly. Can I open an education savings account for myself?

Regardless of your age, you can set up a Section 529 plan for yourself to fund educational expenses now or in the future. You can use the money in a 529 plan to upgrade your skills by just taking a few classes at a qualified college or trade school, or working towards a degree or advanced certificate. What happens to ESA money if not used?

What happens to the ESA if a child doesn't use the money? turns 30,* the unused portion can be rolled over to another eligible family member under age 30. If money remains in the ESA when the child turns 30, the ESA will be distributed and taxable to the child. Can a grandparent open a Coverdell?

In losing control of the account, a grandparent would no longer have the option of transferring the money to a different beneficiary, or of withdrawing the money if needed for other purposes. That said, there is no law that prevents a grandparent from opening a Coverdell account. Is an emotional support animal tax deductible?

For those who have an Emotional Support Animal (ESA), you may be able to claim a tax deduction for the costs associated with caring for the ESA. To take advantage of this pet tax deduction, you must be able to prove that your service animal helps you treat a diagnosed mental or physical need. What is the difference between educational savings account and 529?

Regarding elementary and secondary schools, the important distinction between a 529 plan and a Coverdell ESA is how tuition and expenses are handled. A 529 plan, when used for elementary and secondary schools only, is limited to tuition, while a Coverdell ESA can pay for elementary or secondary school expenses as well. Which of the following is a difference between a prepaid tuition plan and a college savings plan?

Prepaid tuition plans let you purchase college credits or units at today's prices to be used in the future. College savings plans let you invest contributions that can be withdrawn later to help pay for qualified tuition expenses. Are IRA contributions tax deductible?

Your traditional IRA contributions may be tax-deductible. The deduction may be limited if you or your spouse is covered by a retirement plan at work and your income exceeds certain levels. Are education savings accounts taxable?

Advantages are: The earnings are tax-free if used for qualified education expenses. WHO Reports 1099 Q parent or student?

Who uses the 1099-Q for their tax return? Whoever the 1099-Q is issued to must report that 1099-Q on their tax return. In other words, the person whose SSN is on the 1099-Q should report the form – it could be the beneficiary student or the account owner, who may be a parent or other relative. Can education IRA be transferred to another person?

Coverdell education savings accounts, formerly referred to as education IRAs, help families save for future schooling costs by offering tax-sheltered growth. If for some reason your child chooses not to use the money in his Coverdell account, you can transfer it to another family member who is under the age of 30. What is the maximum amount he can contribute to the five esas?

$2,000 per child

What are qualified 529 expenses?

529 qualified expenses. College tuition and fees. Vocational and trade school tuition and fees. Elementary or secondary school tuition. Off-campus housing. Can you roll an education IRA into a 529 plan?

You can't roll over your IRA into a 529 plan without taking a tax hit and, in some cases, paying a penalty, too. Better options include using an IRA distribution to pay for education expenses or funding a 529 with regular income. All 50 states offer 529 savings plans to help families save for higher education expenses. Do college funds gain interest?

Savings accounts in 529 plans can offer higher interest than at the bank, but fees can affect earnings. A parent who deposits $20 earns interest at the same rate as someone who deposited a total of $100,000. Is there a income limit for Roth IRA?

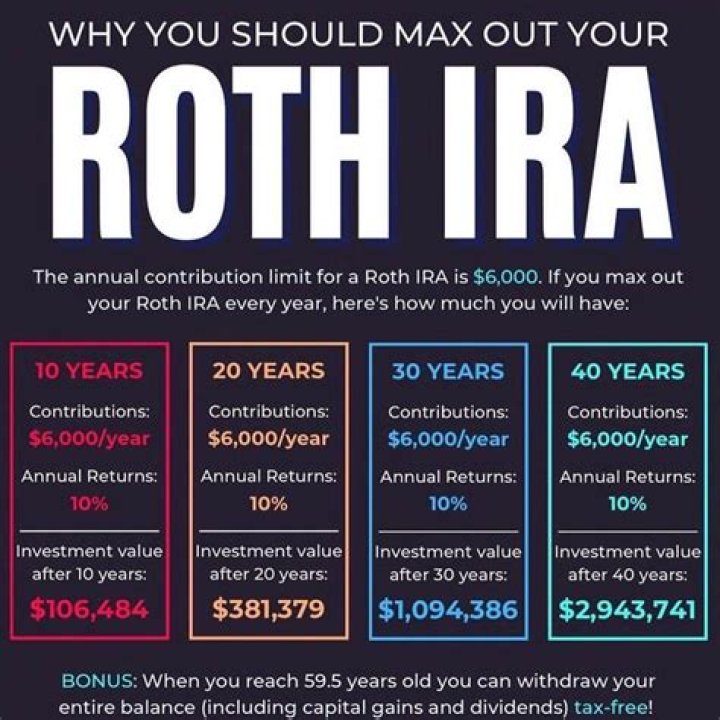

There are income limits for Roth IRAs. As a single filer, you can make a full contribution to a Roth IRA if your modified adjusted gross income is less than $124,000 in 2020. A partial contribution is allowed for 2021 if your modified adjusted gross income is more than $125,000 but less than $140,000. What are the income limits for Section 529 plans?

The Coverdell ESA limits contributions to $2,000 annually and restricts eligibility to those with adjusted gross income of $110,000 or less if single filers, and $220,000 or less if filing jointly. Anyone can open and fund a 529 savings plan—the student, parents, grandparents, or other friends and relatives. Is a Roth IRA a non education IRA?

—Flexibility: Unlike 529s, Roth IRAs permit funds not spent on education to be used for personal retirement. What is a Section 529 plan?

A 529 plan is a tax-advantaged savings plan designed to encourage saving for future education costs. 529 plans, legally known as “qualified tuition plans,†are sponsored by states, state agencies, or educational institutions and are authorized by Section 529 of the Internal Revenue Code. Who qualifies for lifetime learning credit?

To be eligible for LLC, the student must: Be enrolled or taking courses at an eligible educational institution. Be taking higher education course or courses to get a degree or other recognized education credential or to get or improve job skills. Be enrolled for at least one academic period* beginning in the tax year.