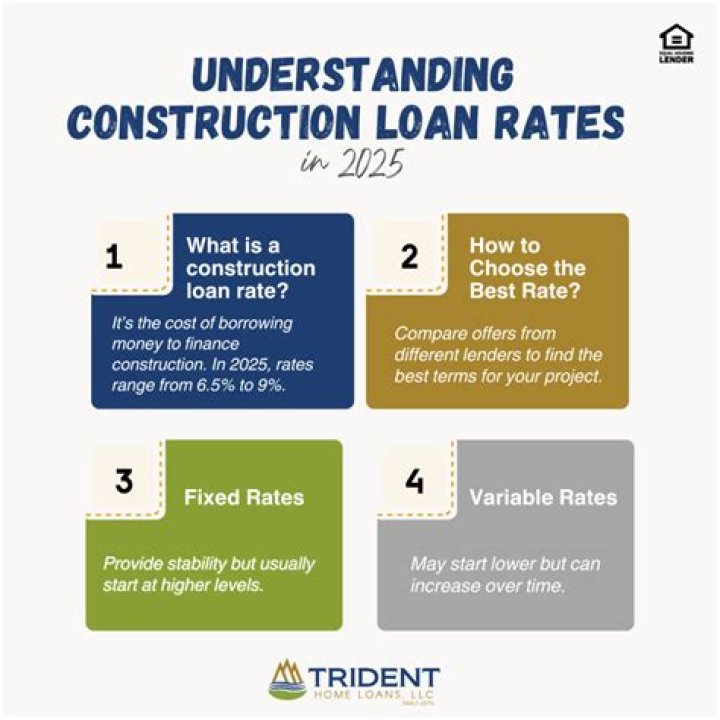

How do you calculate interest only on a construction loan?

- Take 70% of the loan amount.

- Use this calculator to figure out monthly payments.

- Multiply the result by 12 to get the total approximate interest.

Moreover, how do I calculate interest on an interest only loan?

Interest-Only Loan Payment Formula

- a: 100,000, the amount of the loan.

- r: 0.06 (6% expressed as 0.06)

- n: 12 (based on monthly payments)

- Calculation 1: 100,000*(0.06/12)=500, or 100,000*0.005=500.

- Calculation 2: (100,000*0.06)/12=500, or 6,000/12=500.

Likewise, how do I calculate interest only repayments? Divide your interest rate by the number of payments you'll make in the year (interest rates are expressed annually). So, for example, if you're making monthly payments, divide by 12. 2. Multiply it by the balance of your loan, which for the first payment, will be your whole principal amount.

Also question is, how do interest only construction loans work?

During construction, interest-only payments are commonly made on the balance of the money you've drawn. The loan is designed to pay the contractors and subcontractors in regular installments based on how much of the work has been completed at each stage of construction.

Why would you get an interest only loan?

Interest-only loans offer an alternative to paying rent, which can be expensive and uncertain. If you have irregular income, an interest-only loan can be a good way to manage expenses. You can keep monthly obligations low and make large lump-sum payments to reduce the principal when you have extra funds.

Related Question Answers

What is a interest only loan example?

A mortgage is “interest only” if the scheduled monthly mortgage payment – the payment the borrower is required to make --consists of interest only. For example, if a 30-year loan of $100,000 at 6.25% is interest only, the required payment is $520.83.How do you calculate total interest?

How to calculate interest on a loan- Gather information like your principal loan amount, interest rate and total number of months or years that you'll be paying the loan.

- Calculate your total interest by using this formula: Principal Loan Amount x Interest Rate x Time (aka Number of Years in Term) = Interest.

How do u calculate interest?

You can calculate Interest on your loans and investments by using the following formula for calculating simple interest: Simple Interest= P x R x T ÷ 100, where P = Principal, R = Rate of Interest and T = Time Period of the Loan/Deposit in years.What is an interest only loan calculator?

What is an interest-only mortgage? Using an interest-only mortgage payment calculator shows what your monthly mortgage payment would be by factoring in your interest-only loan term, interest rate and loan amount.What is the formula to calculate monthly payments on a loan?

Loan Payment (P) = Amount (A) / Discount Factor (D)- A = Total loan amount.

- D = {[(1 + r)n] - 1} / [r(1 + r)n]

- Periodic Interest Rate (r) = Annual rate (converted to decimal figure) divided by number of payment periods.

- Number of Periodic Payments (n) = Payments per year multiplied by number of years.

What is simple interest calculator?

Use this simple interest calculator to find A, the Final Investment Value, using the simple interest formula: A = P(1 + rt) where P is the Principal amount of money to be invested at an Interest Rate R% per period for t Number of Time Periods. Where r is in decimal form; r=R/100; r and t are in the same units of time.What is the monthly payment on a 20000 car loan?

If you borrow $20,000 at 5.00% for 5 years, your monthly payment will be $377.42. The payments do not change over time.Which bank is best for construction loan?

The 7 Best Construction Loan Lenders- Best Overall: Build Buy Refi.

- Runner-Up, Best Overall: TD Bank.

- Best for Bad Credit: FMC Lending.

- Best for First-Time Borrowers: Wells Fargo.

- Best for Low Down Payment: GSF Mortgage Corporation.

- Best for Low-Interest Rate: First National Bank.

- Best for Online Borrowing: Normandy.

Do you make monthly payments on a construction loan?

Prior to the completion of construction, you only make interest payments. Repayment of the original loan balance only begins once the home is completed. These loan payments are treated just like the payments for a standard mortgage plan, with monthly payments based on an amortization schedule.How much downpayment is required for a construction loan?

Credit score: Most construction loan lenders require a credit score of 680 or higher. Down payment: A 20% to 30% down payment is typically required for new construction, but some renovation loan programs may allow less.How does a builders loan work?

The loan amount is disbursed in instalments onlyUnlike the home purchase loans, where the lender pays the full amount in lump sum, the amount for home loan for construction is disbursed in instalments only. The approved loan amount will be disbursed in phases, depending on the progress of the construction.

How does construction permanent loan work?

Construction to permanent financing is a type of loan which allows you to build or renovate your home. When the construction is done, this loan rolls over into a traditional mortgage without you having to go through another closing. This means you'll only have to pay for one set of closing costs.Can you get a construction loan with 10% down?

Yes, you can get a construction loan with 10% down but it depends on the lender and the program they use. Traditionally financed construction loans will require a 20% down payment, but there are government agency programs that lenders can use for lower down payments.Is it harder to get a construction loan than a mortgage?

Construction loans are short-term.Since there is more risk with a construction loan than a standard mortgage, interest rates may be higher. Also, the approval process is different than a regular mortgage.

What are the qualifications for a construction loan?

What are the Requirements for a Construction Loan?- Credit Score and Income Minimums. As is typical with any type of loan, you'll want your credit to be in tip-top shape.

- Down Payment.

- Creating a Detailed Plan for Your Construction Project.

- Selecting a Builder You'll Work With on Your Project.

- Getting an Appraisal Amount for the Envisioned Project.

Can I get a construction loan with 5 down?

Private lenders may offer construction loans to qualified borrowers with a 5 to 10 percent down payment requirement. Government-backed loans are available with as little as zero down.How long can you have an interest only loan?

five yearsIs an interest only mortgage a good idea?

The advantages of interest only mortgages are: Lower monthly payments because they only cover the interest. More flexibility to choose where your money goes. You could save up enough to pay off your mortgage more quickly or keep a lump sum to buy something else.Who can get an interest only mortgage?

To qualify for an interest-only mortgage, you'll need to prove to your lender that you have a solid repayment plan. This could come in the form of investments like ISAs, or you might have cash in savings or endowment policies. Alternatively, you could sell a second property, if you have one.How is interest calculated monthly?

To calculate a monthly interest rate, divide the annual rate by 12 to reflect the 12 months in the year. You'll need to. Example: Assume you have an APY or APR of 10%. What is your monthly interest rate, and how much would you pay or earn on $2,000?Why is a interest only loan better for an investment property?

It is common for investors to take out interest only loans on investment properties. This allows them to make minimum repayments on tax deductible debt, allowing them to direct more of their income to pay off the loan on their owner occupied property which is not tax deductible.Can you refinance interest only loan?

An interest-only loan is offered for a relatively short term, usually five to 10 years. If you remain in the home, you can refinance the loan into a traditional principal-and-interest mortgage, or sign up for another interest-only term.How is installment amount calculated?

USING MATHEMATICAL FORMULAEMI = [P x R x (1+R)^N]/[(1+R)^N-1], where P stands for the loan amount or principal, R is the interest rate per month [if the interest rate per annum is 11%, then the rate of interest will be 11/(12 x 100)], and N is the number of monthly instalments.